I. Economic Governance

Governance is a conscious management of regimes with the aim of enhancing the effectiveness of political authority, thought of as the applied realm of politics, in which political actors seek mechanisms to convert political partiality into managing society and the economy. Economic governance involves improvements in the technical competence and efficiency under a more accountable, transparent and predictable public policy domain. The missing links in economic governance and participation in the global arena point to the dismal policy performance of states that can be attributed to economic fragility of states. The importance of the missing link in such a convergence of the economic, social, and political schema reflects an emerging consensus on the mutually reinforcing role of these arenas that emphasize the political context of development.

Economic &

developmental agenda focus on rehabilitating the

role of the State in its core regulatory functions and link sustainable

development to political liberalization. Such paradigmatic bonds

notwithstanding, the definition of good governance is mired in the dilemma of

an Africa that is growing rapidly, but the gloomy pace of translating such

growth into sustainable livelihoods can be attributed to state dominance of the

commanding heights. One manifestation of this in Ethiopia is.

On 25 Sept.

2010, the Ethiopian Management

Professionals Association held a Symposium on Management Priorities of the newly re-elected Ethiopian Government - Ethiopia: Public Management Priorities 2010 –

2015 at the AAU CBE campus. At that time, Ciuriak & Previlleit (2010), asserted that as the government

faces the usual panoply of challenges endemic in developing countries. Against

a background of too few instruments and too few resources, it had to grapple

with the perennial problem of managing development: sequencing of policy

reforms, all subject to the political constraints of containing the disruptive

impacts of policy reforms to acceptable levels. Given the very narrow margins

for maneuver imposed by fiscal and external deficits, subsistence levels of

household income for much of the population and a complex ethnic/regional weave

in its social fabric; the long-time co-existence of high inflation rates and low interest rates; this is a particularly important problem for Ethiopia. Getting the priorities right was

the central agenda of the Symposium.

This write up is inspired by the talk of massive

devaluation (22%) devaluation of the Birr on Aug 31, 2010, designed to boost

export performance, represents an important recognition by the government that

its policy setting had been a factor in inhibiting Ethiopia’s balance of payments.

However, by itself, this move fell short of addressing the problem, which

reflected numerous complex factors. In the first instance, given the role that

the exchange rate peg had played in promoting domestic price stability, the series

of devaluations leave open the question whether the strategy will maintain

macroeconomic stability while it seeks to boost export performance. Moreover, it is not out of question that the

devaluation alone might prove to be disappointing in terms of its impact on

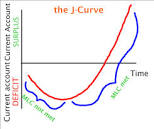

trade performance. In the very short term due to a J-curve response whereby

the trade balance initially deteriorates as import costs are driven up while

the export response is slow to take effect.

II. Policy issues

This article argues that Ethiopia’s trade performance has been held back by a combination of factors that are amenable to policy treatment: very high trade costs, onerous red tape and a confusing macroeconomic framework and policy mix that seem with reach only elude, seems tractable only to resist realization. Similarly, targeted infrastructure and regional cooperation, in conjunction with a trade-friendly macro-economic policy and domestic administrative reforms would, if properly sequenced, enable Ethiopia to use its abundant factor of production: natural resources and cheap labor.

The concerns that

stand out in the latter are, first, the Marshall-Lerner condition states that

the trade balance will correct if the sum of the import and export demand

elasticities is greater than one. In the context of a developing country which

is importing goods for which there are no domestic substitutes, and is

exporting commodities for which demand tends to be price inelastic, the sum of

the trade elasticities may indeed be less than unity. In a developing

country with a highly skewed income distribution, imports are likely to fall

into two broad categories: basic necessities and/or production inputs which

would naturally have low price elasticities and luxury goods, for whom the

devaluation would constitute a relatively minor deterrent. For both reasons, overall import demand may

be quite price inelastic.

Further, market structure may work to dampen the

impact of the devaluation. Commodities produced by developing countries are

often sold into commodity markets dominated by a few major international buyers

whose market power enables them to appropriate the rents; because of this

market structure, it is quite possible for the devaluation to boost the profits

of multinational buyers with little of the benefit trickling down to the

Ethiopian producers. By the same token, this would limit the supply response

and thus the extent of correction in the external balance. At the same time,

given high margins in Ethiopia’s distribution system, import price changes due

to the devaluation may not be fully passed on by importing wholesalers to final

buyers (e.g., if importers seek to maintain volumes on those import items that

are price elastic), which would also work to reduce the overall correction in

the trade balance. Finally, it is important to take into account the impact of

the devaluation on the cost of some of the commodities that are part of the

value chain for domestic production and exports.

III. Policy transfer from IFI

The IFIs (international financial institutions – IMF and World Bank) have been pushing for devaluation incessantly in Africa. From their experience in pushing SAPs through the throat of African states that eventually resulted in dozens of coup d’états, they sure seem to rouse anger in the Ethiopian populace eventually wreaking havoc on the polity.

For example, Ethiopia’s main 'strategic imports' are petroleum products, malt, fertilizer, edible oil, wheat, clothing and industrial goods and machinery for the massive infrastructure development taking place. None is a luxury good that can be curtailed by a devalued Birr. On the flip side, one can ask what rationale can revolutionize the monetary value of raw coffee and sesame in a devalued Birr. Additionally, it is employees with fixed income (government employees, national defense and law enforcement personnel and pensioners) that will bear the brunt of escalating prices of imported basket of basic necessities, goods and services (transport, energy, food, clothing, building materials, house rent, etc.)

Further, the Ethiopian government should not be under duress by the IFIs for a devaluation that has little rationale as has been done in 2010, as stated earlier. That action is one of the measures along with the lack of liberalization of the finance industry, responsible for the GTP I inability to achieve the 14.5% growth predicted. The IFIs should rather focus on macro-polices necessary for private capital to play a more significant role.

IV. National economic management is complex!

Powerful manifestation of this dictum is the fact that getting this process to work undoubtedly reflects the fact that economic development does not just evolve out of Policy Transfers. It is systemic in that it involves the generation of complex features and processes that make up a national economy and the ways in which different segments of the economy are connected of different types of firms interacting with a host of trade partners and building infrastructure and institutions. Ultimately, the outcomes of such an economic alignment will also be responsible to transform the jobs and knowledge base of its workers.Again, while Ethiopia has recorded significant achievements in GDP growth, it faces predictable armor of trials with too few mechanism and wherewithal, while also wrestling with the perennial problem of sequencing policy reforms, all subject to doctrinal reins of the developmental regime dispensation. Accordingly, a more comprehensive policy response of adjusting the monetary policy mix, expanding Ethiopia’s industrial supply capacity and reducing trade costs, policy commitment to enhance the role of the global private sector and confidence building in its citizenry, sustained over the long-term, is required to redress a situation generated by decades of policy settings inimical to good export performance.

When the financial sector is underdeveloped, part of the population operates in a cashless society. Financial and telecom liberalization is an integral part of the overall economic liberalization, a set of policy measures designed to deregulate and transform the system with the view to achieving a liberalized market-oriented system within an appropriate regulatory framework. Findings of the research undergird eloquent testimony of complexity and uncertainty theories and functioning economic models that Ethiopia can emulate, underpinning the fact that this can be complex, when reforms are subject to ideological therapy.

Hence, managed restructuring of the public sector, establishing institutional capacity for policy analysis, formulation and coordination, regulatory capacity, advancing fiscal sustainability and controlling corruption and state excesses are gleaned as a panacea for change and transformation. Creating a merit based and metric civil service is a basic requirement to achieve higher ‘allocative’ and ‘productive’ efficiency, augmenting private sector share and improving public sector financial health. African countries have now deregulated their industry and wooing investors to the economy, with significant impacts to show, driving rapid growth with the exception of some state monopolies.

No comments:

Post a Comment